Here's a new report on the factors influencing drug expenditure, including the issues around pricing. It surely helps politicians and other stakeholders to understand the complexity of the pricing process pharma companies see themselves confronted with.

Recent reports of increases in drug list prices and overall spend on medicines have put the spotlight on the cost of medicines in the U.S. The increasing list prices of specific medicines has, in particular, generated significant media attention. These messages have amplified concerns of policy makers, insurers, pharmacy benefit managers and other healthcare stakeholders that drug prices are to blame for rising costs in the U.S. healthcare system.

However, much of the coverage on list prices has left out the more complex context of the prices, including

prices actually received by manufacturers or paid by intermediaries or patients

the volume usage of the drugs in question

the longer term context of the changes in a drug’s prices over time—including periods of price drops after patent protection

In this report you will find an in-depth analysis of the trends in medicine spending growth and manufacturer net revenues suggesting a far more complex situation than one of prices set by manufacturers simply being too high or growing too fast.

In particular the report highlights the dynamics between prices and volume and introduces a novel way of combining market segments to consider the impact of patent expiry alongside other price related elements. The result is a clearer reflection of trends that affect the costs of medicines in the market. The report also notes that the trend of manufacturer revenues and patient costs are evolving in opposing directions, and that patient exposure to cost trends are not uniformly distributed across patients.

Here's a new report on the factors influencing drug expenditure, including the issues around pricing. It surely helps politicians and other stakeholders to understand the complexity of the pricing process pharma companies see themselves confronted with.

The Quintiles_IMS_insitute published a report on the drivers of drug expenditure in the U.S.

"Much of the coverage on list prices has left out the more complex context of the prices, including

prices actually received by manufacturers or paid by intermediaries or patients

the volume usage of the drugs in question

the longer term context of the changes in a drug’s prices over time—including periods of price drops after patent protection"

I must state: obliged reading for policy makers, insurers, pharmacy benefit managers and other healthcare stakeholders, including journalists (!)

And, still this is not the whole story, of we also look at regulations to access to markets, including reimbursement ruling and influences of reimbursement models/schemes like pay for performance and population health, as well as preference schemes for medicines by medical committees or payer incentives...

Husson: Over the past few years, I was lucky enough to travel to many different places: in most European countries, in the US, in Brazil, in the Middle East, in India, in Indonesia or very recently in Japan and Thailand. The digital revolution is happening all over the place and it is fascinating to see how it is changing people’s habits. In particular, mobile is a game changer in most economies and this will only accelerate. (..)

Significant economic, political, and technology trends will strain global digital strategies further by elevating the importance of local relevance. Over the next few years, we expect the following trends:

Geopolitical shifts drive global fragmentation..

Empowered consumers seek brands who reflect their local values (..)

Innovative local competitors emerge (..)

Mobile’s primacy forces a re-evaluation of local offline marketing(..)

Rise of conversational interfaces reward local knowledge. (...)

To close this capability gap, marketers must evolve their cultural mindset, adapt their organization to share more responsibilities with local teams, implement an insights-driven approach to personalize experiences, and upgrade their global technology infrastructure.

rob halkes's insight:

Unexpected(?) trend in Engaging global brands with local customers/users. Thomas Hudson: ".. counter intuitively, digital complicates global marketing... digital increases customer expectations for relevance, giving local brands the edge. Such competition exposes global brands’ digital marketing gap, forcing them to localize their digital approach." I gathered this before for Pharma companies: Pharma needs to differentiate to local! See https://lnkd.in/gqb86hV - and here: https://lnkd.in/eDMsDdr .

While the level of drug expenditure is closely watched and often commented upon, the composition of that expenditure and its dynamics are less

This report describes the dynamic changes in the composition of drug expenditure over the period 1995 to 2015 for five developed countries—France, Germany, Japan, the United Kingdom, and the United States. Over the past 20 years, therapies that once dominated spending are now dramatically less important, while other entirely new therapies have risen to a significant share of spending.

Key insights include:

Nominal drug expenditure measured at invoice price level has risen substantially over the past 20 years across all countries analyzed, though less so when normalized for economic and population growth.

When composition of drug expenditure is examined, the classes that dominated spending 20 years ago have shrunk considerably as innovation and product lifecycles shift costs downward.

Older therapies have declining importance as many have lost patent protection and costs have reduced considerably, while others have seen continuous innovation and have risen in share of spending.

Across all five countries, some common patterns emerge in terms of the therapy areas that now make up the large portion of spending and those that have declined. That said, each country has a distinct set of dynamics, spending compositions, and underlying clinical, disease, and policy drivers.

Some noteworthy conclusions at the summary of the report on drugs spend in period 1955 - 2015:

"Nominal drug expenditure measured at invoice price level has risen substantially over the past 20 years across all five countries analysed - France, Germany, Japan, the United Kingdom (U.K.) and the United States (U.S.) - but less so when

normalized for economic and population growth and especially in the most recent decade.

By contrast, drug spend has not risen as rapidly as a percentage of health expenditure, and for some countries has declined from peaks in the late 1990s.

The amount of spending for new branded drugs – those on the market for less than 2 years in that country – is generally less than 10% of spending in all countries analyzed. At least 60% of drug utilization by patients are drugs that are generic or do not require a prescription."

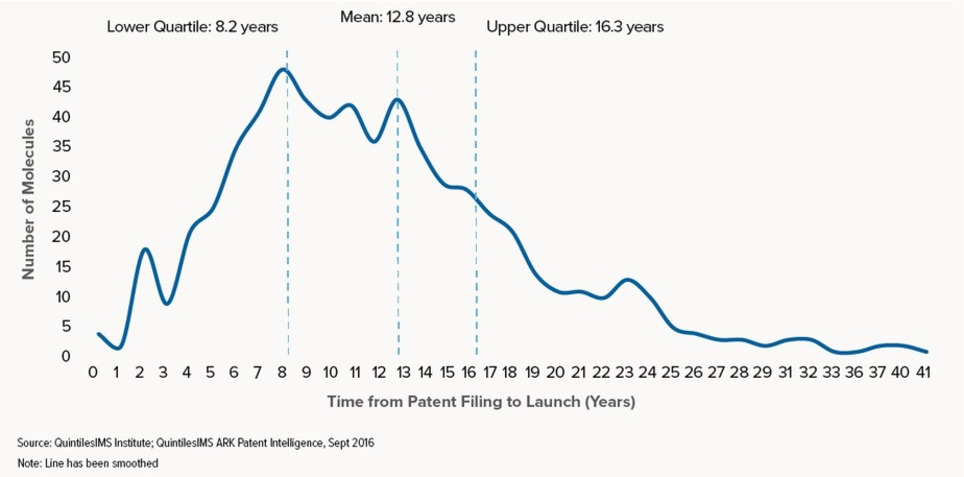

This report profiles the NASs launched in the U.S. over the past 20 years and measures the length of a molecule’s lifetime from patent filing to launch and eventual patent expiry. It also explores the significant variations in this lifetime when viewed by molecule characteristics such as therapy area, orphan drug status, and the type of companies involved in the development and marketing.

Take a look at some of the coverage from the event in The Scientist, American Journal of Managed Care, and The Pharma Letter.

rob halkes's insight:

Relevant Insights into the development in lifetime characteristics of biopharmaceutical substances: only relative few outliers that make a quick retunr about 1$ billion a year (within 5 years after launch) Modest levels of average return (less than $100 billion) a year for 62% of launches in the past 20 years. The commercial returns for a small number of outlier molecules areoutsized but rare, while a substantial number of molecules baing launches achive levels of commercial success that fall far below threshold levels of economic return.

Pharmaceutical manufacturers, payers and healthcare providers (HCPs)—as well as a host of tech-focused newcomers—are exploring digital programs that complement standard therapies and hold promise to keep patients healthier and produce better outcomes. Known as “beyond-the-pill” or “around-the-pill” services, they have been a long time coming, and may finally be gaining traction, according to a new eMarketer report,“US Healthcare Beyond the Pill: Digital Tech and New Partnerships Bring New Life to the Industry” (eMarketer PRO customers only).

For the past several years, healthcare and pharma firms have been trying, with mixed success, to step up their beyond-the-pill programs. Early efforts included basic informational websites and simple apps designed to provide information about medical conditions and therapies.

“When the pharma industry first moved into digital technology, it was primarily in the marketing space, leveraging things like websites or HCP portals to share product information and to educate,” said Amy Landucci, head of digital medicine at Novartis. “But in the last three years, we’ve seen a pretty big shift away from just doing digital marketing—though it’s still very important—to looking at how technology can help enhance patient outcomes.”

Today’s beyond-the-pill solutions can collect, monitor and analyze health-related information, track patient activity, improve medication adherence, provide personalized decision support, predict medical crises and streamline medical care using a variety of advanced computing techniques. Mobile technology, the IoT and AI are three of the technologies making this possible.

Pharma started about thinking in terms of servicing health care "beyond the pill" in about 2000. Today developments have been increased by ideas of 'integrated care' and "precision medicine" the latest concept indicates fine tuning of medications to personal physical and genome conditions. Diagnostics are all in the game, that is. But a study in which I participated [ http://1.eyeforpharma.com/LP=5676 ] made clear that development and creation is one, servicing and delivering is two. Partnerships for example are unavoidable is one in in the game for sustainable business.

Join Murray Aitken and Michael Kleinrock for a webinar on December 8th to discuss findings from the much anticipated Global Outlook for Medicines through 2021 Report (to be released December 6th).

During the webinar, they will share an updated perspective on - and the implications of - the use of new and existing medicines as well as spending levels and access constraints through 2021. The report focuses on a global view of the markets for all types of pharmaceuticals, including small and large molecules, brands and generics, those dispensed in retail pharmacies as well as those used in hospital or clinic settings.

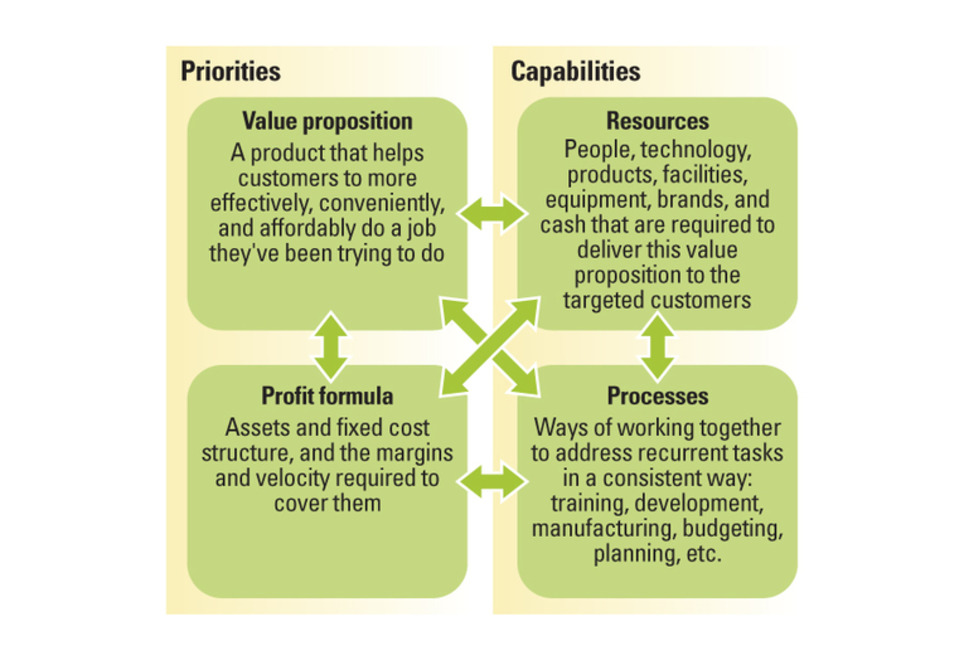

Successful business model innovation requires an understanding of how business models evolve.

Many attempts at business model innovation fail. To change that, executives need to understand how business models develop through predictable stages over time — and then apply that understanding to key decisions about new business models.

Understanding the interdependencies in a business model is important because those interdependencies grow and harden across time, creating another fundamental truth that is critical for leaders to understand: Business models by their very nature are designed not to change, and they become less flexible and more resistant to change as they develop over time. Leaders of the world’s best businesses should take special note, because the better your business model performs at its assigned task, the more interdependent and less capable of change it likely is. The strengthening of these interdependencies is not an intentional act by managers; rather, it comes from the emergence of processes that arise as the natural, collective response to recurrent activities. The longer a business unit exists, the more often it will confront similar problems and the more ingrained its approaches to solving those problems will become. We often refer to these ingrained approaches as a business’s “culture.”

rob halkes's insight:

Great article about business model innovation. I was struck by the resemblances of errors made at introducing new value added services to pharmaceuticals, "beyond the pill". The same may possibly be expected by the new "hype" (?) about patient centricity: in my mind doing things without reflection about what it is: ending up in webinars/conferences existing mainly of either pharma staff in which they share their ignorance, or even in pharma staff added with a patient or patient representative, in which the patient is commonly canonized (as in 'sainted'): understandable but not a functional way of developing new trends in a company, let alone a new trend in a business sector..

See here what patients really have to say about corporate pharma companies and its patient "centricity": PatientView.com

Based on EvaluatePharma’s coverage of the world’s leading

5,000 pharmaceutical and biotech companies, the World Preview highlights trends in prescription drug sales, patent risk, R&D spend, global brand sales and market performance by therapy area.

If there was any doubt that the pharmaceutical industry is entering a period of sustained growth it should be put to rest by this year’s World Preview 2015 showing prescription drug sales are set to advance at almost 5% a year until 2020.

Continued confidence in the sector is being driven by a number of positive fundamentals including the recent increase in R&D productivity, which has resulted in a big hike in drug approvals, and the emergence of breakout drugs such as Gilead’s Sovaldi franchise. Excitement surrounding new products including Merck & Co’s Keytruda, Bristol-Myers Squibb’s Opdivo and anti-PCSK9s from Amgen and Sanofi should ensure the sales momentum continues.

The current industry feel-good factor has also been mirrored in the amount of money businesses are raising, the number of pharma and biotech companies floating on exchanges around the world, and the healthy appetite for M&A seen across the board.

While some things are changing in the industry, others remain the same. A strong focus on oncology has helped Novartis retain its crown as the number one pharma company in terms of prescription sales. More interesting, however, has been the rise of ‘big biotech’ and specialty pharma into the ranks of the industry’s big players.

Despite setbacks from some approved and clinical biological drugs depressing the speed of change, the global sales contribution from biologic drugs is forecast to jump from 23% in 2014 to 27% in 2020.

These drugs have traditionally enjoyed greater patent protection than their small molecule relatives,but the landscape is changing with the approval this year of the first US biosimilar

Future outlook

Standing at the midpoint of 2015, the pharma and biotech industry looks as if it is in very good shape, the patent cliff is firmly in the rear view mirror, and while it might be too early to call on sustained R&D productivity, things are at least moving in the right direction. The only clouds currently on what looks to be a sunny horizon for pharma and biotech are global pricing

and market access. With many predicting that for the first time the industry could produce a series of real ‘cures’ for previously intractable diseases, it is clear that these innovative drugs will come at a price. What is also clear is the growing reluctance of both government and private healthcare providers to fund very expensive drug treatment regimens

Complimentary copies of the full report can be downloaded at:

Looks like the pharma business awaits a fruitful future. However dark clouds are emerging at the pharma skies too. Challenges to business and commercial approaches might not only concentrate on pricing, but certainly, with a rising trend in a demand for increasing health outcomes of medication, on the right applications and adherence too. Partnership with healthcare providers that goes beyond 'just' delivering drugs seems to become crucial.

Big, multihospital health care systems increasingly dominate the US market, and they are reshaping where and how vendor selection is made. Many medical-technology companies are not fully prepared for the changes taking place in purchasing dynamics. Companies that develop a top-quality KAM function will build a powerful advantage.

In this article:

US hospitals continue to consolidate, concentrating the power of big health systems over purchasing decisions.

Selling successfully to these organizations requires a deep understanding of their strategy, stakeholders, and decision-making processes.

The challenge is building an account team with requisite in-depth customer knowledge, which requires a key account management approach and an exceptional degree of coordination across a vendor’s selling resources.

A New KAM Model: From Sales Transactions to Strategic Partnerships

Main take aways:

- Centralization of purchasing is on the rise, but the structures and processes vary. The shift of purchasing authority for medtech products from clinical to economic decision-makers is well recognized. Less well understood are the structure and hierarchy in which purchasing decisions are made at each large system and the often complex role of national, regional, and local value-analysis committees. - Health system value-analysis committees rank clinical value over clinical preference. Value analysis—measuring the benefits of a device relative to its cost—has resulted in more informed and more economically sophisticated decision-making in large systems. Physicians are increasingly “picking their battles” instead of fighting hard for every clinical preference

- Develop customer-specific account plans that are built upon deep customer understanding. Best-in-class account plans reflect a deep understanding of a customer’s business strategy and objectives—and extensive knowledge of the customer’s purchasing process and key decision makers.

The challenge for medtech account teams is determining where the purchasing authority resides in each system’s structure and understanding what factors those decision makers care most about. Good account plans use this understanding, as well as a detailed analysis of the customer’s market position, market share, and growth prospects, to help articulate a clear sales strategy and how that strategy will help the customer achieve its objectives. Periodic reviews, especially after a significant customer event such as a merger, acquisition, or senior-management change, help keep the sales strategy fresh and relevant.

- Develop clear economic and clinical value propositions for core products. Medtech suppliers need to demonstrate the value that their products can deliver beyond price and clinical efficacy. Potential proof points are improving outcomes, increasing workflow efficiency, requiring fewer staff, reducing infections, adding new profitable patients, reducing readmissions, and many more. - Adopt a consistent and defensible national pricing and contracting strategy.

- Implement a sales coverage model that defines clear roles for key account managers and sales reps in the field. The most progressive medtech companies are beginning to vary their sales coverage on the basis of customer characteristics.

-Build a KAM team that possesses a new set of skills

- Provide the team with management tools that support efficient decision-making and cross-functional sales execution.

rob halkes's insight:

BCG has found out about the same as I did already since 2007: Key Account management demands crossfunctional teams, "build on the basis of customer characteristics", not only according to quantitative parameters but also on qualitative characteristics, I would add! See a summary of my experience here.

Do have me explain to you what experience tells about how to set this up!

The first half of 2015 continued to confound the naysayers of the pharma industry, with deal making, venture funding and share price indices all showing no signs of slowing down, according to EP Vantage's Pharma & Biotech Half-Year Review 2015.

Key highlights

The year started with one of the biggest venture rounds ever with the $450 million Moderna Therapeutics managed to secure from its investors in January

VCs gifted $3.8 billion to companies at the half-year point signifying that 2015 could once again raise the bar in terms of funding totals

On average, the 32 floats in 2015 yielded only a three percent discount from the listed range, and increased in value by 23 percent since their IPOs

See download the report

rob halkes's insight:

If pharma approaches the business wisely and with willingness and capacity to innovate, then there is a lot still to be done and gained.

The market for digital dose inhalers for asthma and COPD will be worth $3.56 billion in 2024, according to a new prediction from Grand View Research.

Though connected inhalers are a new market, they've seen rapid growth in the last few years with interest from big pharma companies like AstraZeneca and Novartis, major device companies like Philips Respironics, as well as the newer, smaller players like Propeller Health that have made a big bet on the space.

Grand View sees that growth continuing into the next several years, citing an aging population and a surge in the prevalence of chronic respiratory disease as two drivers. They also foresee rapid growth for markets outside North America. The firm predicts the Asia Pacific region will grow at a 17 percent compound annual growth rate (CAGR) between now and 2024.

"As a result of impactful economic developments in the fast emerging countries, such as China, India, Brazil, Philippines, and others, there has been growth in the per capita income, which is thus expected to influence the demand for the technologically advanced respiratory devices," the firm writes in a press release. "Moreover, these technology-enabled respiratory devices are greatly sought after among the pediatric and the geriatric population so as to improve the patient medication compliance, dose tracking, and to enhance patient-healthcare practitioner connectivity that would enable real-time tracking of healthcare data; these serve as high impact rendering factors, significantly driving the market growth in the next nine years. [...]

The report names some major players in the space which include a number of companies MobiHealthNews has written about over the years, including Teva Pharmaceuticals, which bought into the space with its acquisition of Gecko Health; Opko Health, which acquired Inspiro Medical; AstraZeneca, a major investor in Australian smart inhaler company Adherium; and Propeller Health, which makes inhaler sensors for a growing number of pharma and provider partners including GSK and Boehringer Ingelheim. They also name Philips Respironics, Novartis, and Glenmark Pharmaceuticals. Glenmark launched a digital dose inhaler, which tracks usages digitally and alerts the user when it's close to empty, in May. Novartis announced in January that it would work with Qualcomm Life on a connected inhaler for COPD.

Smart inhalers might as well be the leverage of pharma to really consider and develop partnerships to healthcare. Delivering inhalers should be more about developing co-creative collaboration and taking responsibility of health therapies in action. Curious how this development will change the pharma/health market! See the customer centric pharma business model as well!

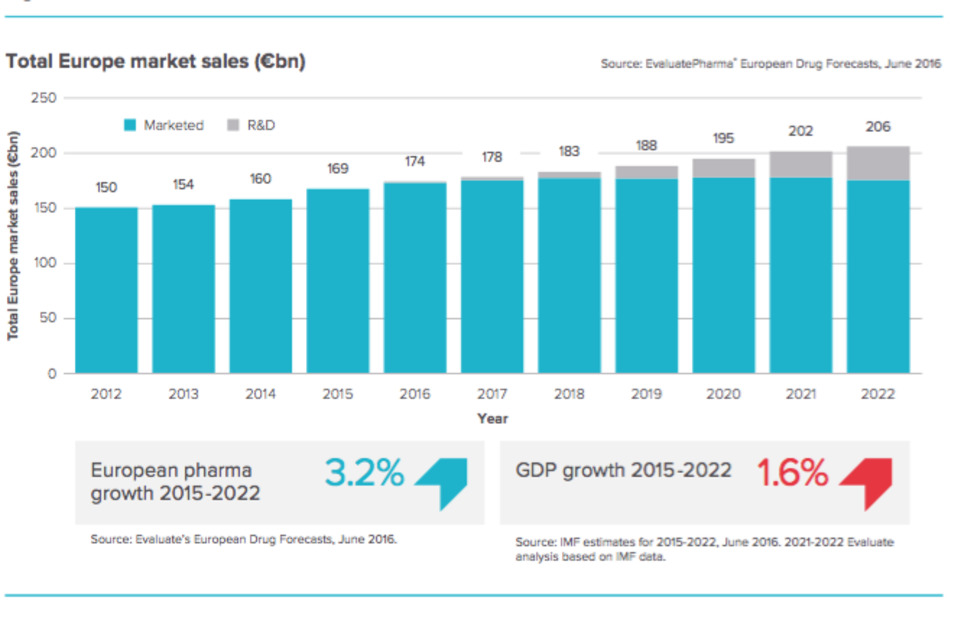

Pharmaceutical Innovation in Europe New pharmaceutical breakthroughs approaching – is the system set up to fund them all?

This report shows that the advent of new potential blockbusters in Europe is expected to position the European pharma industry with increased growth through to 2022 of 3.2% CAGR (2015-2022).

Are healthcare systems and payers ready for innovation?

The pharmaceutical industry has been going through a period of radical transformation of its business model which, coupled with scientic advances, is now resulting in a new wave of innovative treatment options that are anticipated to put additional pressure on the nancial resources of already cash-strapped healthcare systems.

If in the past the balance was primarily achieved via price-cutting policies either supported by the introduction of cheaper generic or biosimilar versions, forced rebates at national level or the application of international reference pricing rules, such a trend is no longer sustainable. It is probably time for payers and the pharmaceutical industry to work together at the same table and devise new and more e cient funding methods as opposed to the often theoretical risk-sharing and pay-for-performance schemes that have been trialled so far.

Report Author:

Antonio Iervolino – Head of Forecasting Antonio.Iervolino@evaluategroup.com

We're getting near the end of the lifetime of the traditional business model of the pharma industry. Blockbuster get scarce and personalized medicine will limit Rx of innovative drugs to smaller groups of patients.

Besides these, commercial challenges are high to traditional companies: information of physicians is not only limited by engagement ruling and closing doors to reps, but it also demands now complicated data based engagement models to create customized journeys of information for target groups via multiple and new channels.

These challenges go together with highly impacting changes of

refocusing to newly targeted customers, by quantitative and qualitative parameters;

new patterns of cooperation between departments within focused account teams;

alignment to the (key) customers' level of health care development into patient's pathways, as key criterion for customer relations development;

collaboration with patient (groups) to help co-create innovation in healthcare;

and servicing customers and patients with added value to better care with lower costs.

Although this seems hardly feasible to do for a centralized pharma company, there are indeed ways to do so, as we experience it. See here for a general introduction:

Germany's Boehringer Ingelheim is to cut more than 700 jobs across its US operations, with the axe falling hardest on its sales functions.

The 724 redundancies include 49 at the company's US HQ in Danbury, Connecticut, but according to a filing with the Connecticut Department of Labor the remainder will mostly occur in sales.

The nature of pharma sales has been changing over the last decade or so, with many companies opting for less face-to-face interaction with physicians and other healthcare providers.

Patent cliffs have also hit big pharma hard, with several firms recently announcing major restructures in a bid to make savings and funnel money into R&D.

Boehringer said in a statement: “The actions we are taking now will help us reinvent the way we serve the needs of our patients, and enable us to continue to make significant investments.”

Boehringer has made a number of recent changes to its operation worldwide in a bid to make itself more competitive. Last year the company announced it was to leave the generics sector by making an asset swap (consumer health interests in return for an animal health business) with Sanofi and a $2.6bn deal with specialty firm Hikma.

From this month Boehringer's R&D operations are to be renamed the 'Innovation Unit', handling all stages of development up to clinical proof-of-concept. Its Prescription Medicines Business Unit will be responsible for the subsequent 'highly market-oriented development' of products.

The US pharma industry has been hard hit in the last year, and the company is not alone in making cutbacks. As part of a move to save $1.5 billion worldwide, AstraZeneca has already pledged to close a manufacturing plant in Westborough, Massachusetts. Other measures will involve shutting a site in Bristol, UK.

… and Arena also plans US and Swiss cuts Meanwhile Arena Pharmaceuticals is also slashing headcount at its workforce in the US by 35% - around 80 staff - in a bid to save $11m. Arena also said it was to make “reductions” at its Swiss manufacturing facility to create further savings.

Harry Hixson, Arena's interim CEO, said: “This initiative supports our strong desire to create a more streamlined and efficient organisation focused on key priorities designed to add both near- and long-term value to the organisation.”

rob halkes's insight:

The new pharma business model does certainly something to the REP! Multi-channel and Account management will overtake their place. However, innovating pharma sales, will not do the trick by just changing it to multi-channel. A new thought through approach needs to focus on accounts based on chances for success, adapt to the level of account relations and must add value that is specific to the customer's development of care. A challenge! Connect to be explained in depth: http://bit.ly/pharma_business

Pharmaceutical companies can play a central role in the digital revolution of healthcare. But capturing this opportunity requires identifying the right initiatives. A McKinsey & Company article.

Pharmaceutical companies are running hard to keep pace with changes brought about by digital technology. Mobile communications, the cloud, advanced analytics, and the Internet of Things are among the innovations that are starting to transform the healthcare industry in the ways they have already transformed the media, retail, and banking industries. Pharma executives are well aware of the disruptive potential and are experimenting with a wide range of digital initiatives. Yet many find it hard to determine what initiatives to scale up and how, as they are still unclear what digital success will look like five years from now. This article aims to remedy that. We believe disruptive trends indicate where digital technology will drive the most value in the pharmaceutical industry, and they should guide companies as they build a strategy for digital success.[ ..]

Trends reshaping healthcare Outcomes based care is moving to center stage [...]

Patients are becoming more engaged [...]

New competitors are moving in [...]

More information is available about product performance [...]

Process efficiency and agility is improving dramatically [...]

Four areas of Digital Opportunity

Against this backdrop, we believe there are four main areas where digital developments will drive value for pharma companies, building on what we see as the key components of digital success—an ability to deliver more personalized patient care, engage more fully with physicians and patients, use data to drive superior insight and decision making, and transform business processes to provide real-time responsiveness.

Companies do not have to become leaders in all four areas across the enterprise—some will deliver more value than others in relation to any given disease, depending on market dynamics and their portfolio. But to decide where to concentrate their efforts, they do need to develop a point of view on each area’s potential to transform their commercial and innovation models. To help in these decisions, we sketch here a picture of how we believe successful pharma companies will operate in each area in the near future.

Capturing the value

Most pharma companies have started to build some digital capabilities, but talent and resources for their efforts can be fragmented, often across hundreds of small initiatives. Without clear strategic direction and strong senior sponsorship, digital initiatives often struggle to secure the funding and human resources required to reach a viable scale, and they cannot overcome barriers related to inflexible legacy IT systems. Talent and partnerships are also critical issues—many companies realize they need to form partnerships to acquire digital capabilities and specialist skills but are often unclear about what kinds of partnerships to set up and how to extract value from them. Read on at the original!

rob halkes's insight:

Pharma has to know explcity how "digital" is going to support their strategic developments, internally and externally. This article by McKinsey (mid 2015) declares how several market developments causes the need for digital. It will be in the "how" that a feeling of being disrupted will emerge. But a wisely designed implementation and development process will create miracles. Specifically so with an outcome at patient level. See some necessary steps here

John Mack, better known as @Pharmaguy from Pharma Marketing news asked me to have an interview with me about this new commercial model for pharma, working customer centric.

We don’t have a transcript of the interview, but do like to present our preparing notes for the interview, which might enlighten some of the key points of the new customer centric pharma market approach:

Starting Point: Pharma’s standard approach to all markets cannot go on as we do; In general: we all know the genera threads to pharma markets, like loss of “blockbuster products”, limited access for promotion to Rx, pricing pressure, inroad of generics, new stakeholders, etc. These are specific to all markets – And what’s more market conditions like access, regulations, promotional rules, preferences, prescription routines, etc. do make all markets differ substantially from each other, even within countries we have regions with their own health policy: e.g. Spain, France, Italy, or even onto local committees like in the UK and the Netherlands.

Need to look at new commercial models adapting to the different market conditions! How to localize/differentiate the market approach?

…

Read here for:

- The starting point ..

- Strategic Positioning

- Building partnerships, and

- the market approach ...

rob halkes's insight:

In a nutshell, I blogged the essential aspects of the new customer centric market approach for pharma in 2013. It is still significant today, even more when we want to help our customers to help their patients better.

In these exclusive videos eyeforpharma's Paul SImms spoke with Eduardo Sanchiz and Alfonso Ugarte, resp CEO and Senior Director of Global Business Units of Almirall, on the changing pharma landscape, patient value and rewriting the business plan.

rob halkes's insight:

Inspiring to see the leadership of Almirall speaking about their personal drives to lead their company to patient centricity.

GlaxoSmithKline, AstraZeneca and Johnson & Johnson have joined with three leading British universities to create a new 40 million pounds ($57 million) fund backing early drug research.

rob halkes's insight:

New pharma cannot do without collaboration and co-creation - not only though in research. The connection with stakeholders to create sustainable care is waiting to be developed.

"Ensuring a change for the better" A Revolutionary Paradigm Shift in Big Pharma's Organisational Development by Cristina Falcão - A paradigm is the conceptual framework upon which we build our world; it is built upon past experiences; if we are not willing to make shifts in our paradigms, we will remain stagnate in our growth a paradigm shift is a change from one way of thinking to another; it is something that does not happen like self generation it is driven by change.

Culture change is not simply about how we see others and ourselves. It is about how the system works, i.e. how we do the work together, rather than how we work together. The paradigm shift is to understand how to act on the organisation as a system.

The most critical thing to understand about a paradigm is that, in a paradigm shift, everything goes back to zero. What does that mean? It means that whatever made us successful in the old paradigm may not even be necessary in the new paradigm....

What Has Changed? Everything – 2012 Portrays Big Pharma’s Future Scenario

Governments around the world are grappling to arrive at solutions for health account deficits. Political pressures have increased during the economic crisis.

Personalised medicine means changing drug portfolios from primary care driven blockbusters towards specialties, where the medical need is so high that regulators are more ready to accept the prices. Evidence of the value that medicines bring to healthcare systems will be required to achieve access and funding in both developed and emerging markets.

However, changing portfolios to address the changing pharma landscape is not enough; the pipelines are dry and R&D costs continue to skyrocket - the new paradigm is not about portfolios. Broadly, to raise innovation returns back to the level that prevailed in the era of blockbusters, pharma companies need transformational change.

Already in 2012, change was needed to pharma's business model. Nowe we see the urge to incrfease by heavy debates on pricing of drugs and generall influences of pharma industry on prescription.

Tghe time has come to act. Not just by changes to the commercial approach, like multi channel management, or other add ons to the traditional promotion, but a rethink and design of the proper approach. See my work on pharma here

For years, there has been a push within the pharmaceutical industry to move “beyond the pill” — in other words, to build and deploy complementary services and solutions to diversify revenue sources. The rationale is simple and elegant: A company with experience selling pharmaceutical products should be able to successfully and profitably sell its large customers (health plans, delivery systems, and governments) other health care offerings.

The impetus to move beyond the pill typically arises from one or two realizations: 1) medicines alone are often not enough for patients to achieve optimal clinical outcomes, and 2) as pharmaceutical pipelines dry up, beyond-the-pill businesses can be valuable new sources of revenues.

However, many beyond-the-pill efforts have sputtered or died. During my years working as a pharmaceutical industry executive and advisor to senior management, I have observed that these initiatives typically fail because of one of three challenges:

Leadership.[..]

Regulatory environment. [..]

Access to capital [..]

Recruit industry outsiders [..]

Form partnerhsips [...]

Revise regulations [...]

Avoid stand alone solutions [...]

Integrate clinical trials [...] The world will continue to need companies that develop and commercialize new medicines. Those same companies must not lose sight of this fact and recruit the right leadership to use around-the-pill services, solutions, and tools to enhance the clinical effectiveness and commercial success of their core products...

rob halkes's insight:

Inspiring article Sachin. Good to see how your experience in the field made you pick and select the best tips to go beyond the pill. We just finished a study about the activities taken by Pharma companies to go this way. Some of your tips are being underscored by the findings, others demonstrate how it is not an easy task from the perspectivce of the traditional blockbuster business model. One of the major conclusions is indeed that knowledge about what added value might be in healthcare and what the difference is between products, services and solutions are key. Besides, and even more so: development and testing services and solutions is one thing: delivering is quite a different game. Not only does the very intention impact the demands to customer relationships: how they are developed into a conditional quality of such relations, but the question of how to get revenue for the added value is quite a challenge. These things have to be thought through before scaling solutions/services to be sure about reimbursement. See here for the study report: http://social.eyeforpharma.com/content/value-added-services-2015 Rob Halkes @rohal

AstraZeneca is diving deeper into personalized healthcare with two projects that move the concept beyond cancer into respiratory disorders and heart disease.

Personalized or precision medicine, which tailors treatment to a patient's genetic profile, is an increasing focus for drug companies, especially after an initiative from U.S. President Barack Obama in January.

Until now, however, the focus has been on cancer, where genetic mutations are well-known drivers of disease.

"The time is now right to extend the personalized healthcare approach and the benefits it brings to all of our therapy areas," Ruth March, who heads the initiative at the British drugmaker, told reporters.

"Up to now the science of personalized healthcare has been slower to reach those common disease areas such as cardiovascular and respiratory disease."

To redress the balance, AstraZeneca said on Wednesday it had signed two deals, one with Abbott Laboratories for a diagnostic test to accompany an experimental asthma drug and another with Canadian scientists on genes associated with heart disease.

Abbott will develop a diagnostic test to identify patients with severe asthma who are most likely to benefit from AstraZeneca's new antibody drug tralokinumab, which is in final-stage Phase III clinical tests.

To date, there are no such approved blood tests for use in asthma.

A separate tie-up with the Montreal Heart Institute will screen samples from up to 80,000 patients for genetic traits linked to cardiovascular disease and diabetes, in a program that may help doctors work out which patient should take which drug.

By 2020, AstraZeneca expects half of its new drug launches will come with so-called companion diagnostics to identify those patients most likely to benefit from different treatments.

This approach is already used in cancer, with Roche's breast cancer drug Herceptin and AstraZeneca's lung cancer medicine Iressa, for example, given to patients with particular genetic profiles. Cancer has long been a key area for AstraZeneca, which was the target of a $118 billion attempted takeover last year by Pfizer.

Along with rivals in the field, AstraZeneca will showcase its latest cancer drug advances at the May 29 to June 2 American Society of Clinical Oncology (ASCO) annual meeting in Chicago.

Industry analysts say most attention will be focused on the latest clinical data on AstraZeneca's combination of two experimental medicines, MEDI4736 and tremelimumab, in treating lung cancer.

rob halkes's insight:

As we have noitfied in researching the developments of Pharma into Value Added Services (see here ), pharma companies are working to see how they can develop services to thealth care that could help the development of integrated care. One aspect we have seen accentuated by the interviewees was the necessity to create partnership with other stakeholders to combine needed competencies. AstraZeneca shows this by their latest partnerships with Abbott Laboratories and the Montreal Heart Institute. Beleive me: health care won't be the same anymore - although there is still along way to go!

3 tailored roadmap's to solutions in healthcare beyond the pill.

- Understand the creation of successful services by looking at organizational structure and internal processes, how to partner with external stakeholders, and how to make projects economically viable.

- A roadmap tailored to your company with three scenarios for creation, development, implementation and up-scaling of ‘Value Added Services’.

- In-depth case studies of company-wide initiatives and specific projects, such as Janssen Healthcare Innovation, Sanofi Integrated Care, Pfizer Integrated Health, Grunenthal´s ‘My pain feels like’ and Boehringer-Ingelheim´s ‘Picasso’.

rob halkes's insight:

I was as happy to conduct the research for Eyeforpharma's Value Added Services Report. It changes the view on how pharma could integrate its different market approaches to focus and be more effective. Effective: both in services to customers and patients, and in commercial return.

I gave already some presentations and workshops to interested audiences, e.g. see here

In 1948, the year I was born, the average American man did not retire at age 65. He died of a heart attack.There were no thrombolytic drugs to break up the clots that were starving his heart of oxygen, no beta-blockers to ease the strain on his heart. There were no cardiac surgeons. Coronary artery bypass grafts lay a dozen years in the future, and though cardiac catheterization had just been developed, it would be nearly three decades before it would be used to reopen blocked coronary arteries

rob halkes's insight:

Pharma matters, in the past, at present and certainly in the future..

But how to define thier new position in healthcare: is it less or more than 'just" making new drugs??

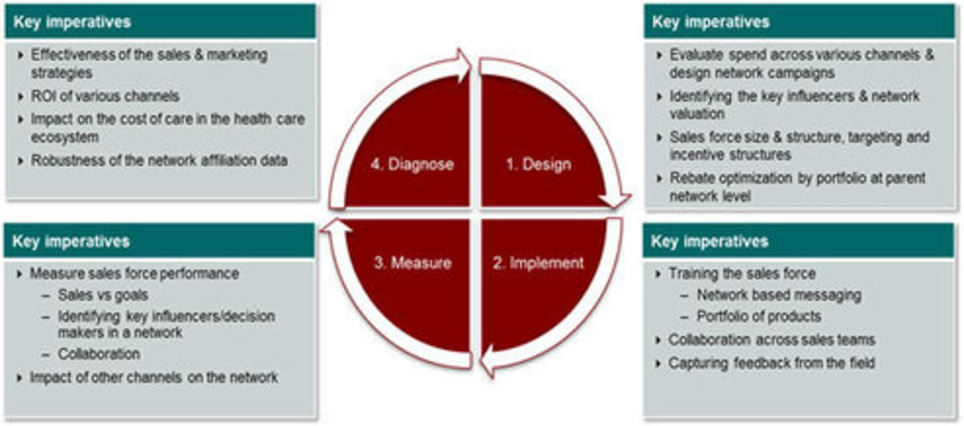

Integrated Delivery Networks (IDN) has resulted in a consolidated network for healthcare providers. Check out how this influences the decision sciences methodology for pharmaceutical companies.

Why this is important

Health care providers are undergoing a series of integrations that result in a consolidated network providing affordable and quality medical care –The IDN. Pharmaceutical companies need to evaluate their sales and marketing efforts and shift their focus from physician based selling to network based selling in order to tap the centralized decision makers.

Conventional Wisdom

Over the past few years the pharmaceutical industry has viewed Physicians as one of the dominant entities influencing its success and growth. A physician reserved the autonomy on decisions concerning the choice of therapy for his patients and was subjected to influence mainly by peers (group-practices) and Industry leaders (KOLs). Consequently, all pharmaceutical companies focused their promotional and educational initiatives on physicians. Sales teams were determined to acquire the mind share of physicians which resulted in having to tap a large group of individuals in order to expect returns. However, this is becoming old school.

The Evolving Industry

In the recent past, Health Care providers (primarily hospital chains) have undergone a series of vertical and horizontal integrations. Vertical integrations included the acquisition of primary care physicians (PCPs), strategic alliances with physicians in physician-hospital organizations (PHOs) etc. On the other hand, horizontal integrations involved the establishment of multihospital systems, alliances with neighboring hospitals and mergers. Over time, such integrations have evolved and enhanced to what is today referred to as the Integrated Delivery Network (IDN).

The integrations have resulted in the creation of a network of facilities and providers working together to offer a continuum of care. Prevailing economic market conditions and an array of healthcare reforms demands high quality of treatment at reduced costs (PPACA -2014). The very nature of integration allows IDNs to gain perspective on quality and cost factors that lead to better outcomes. This new vision focuses not only on intervention, but also on prevention and wellness, guiding patients to the most appropriate site of care, at the right time and cost. In short, IDNs are “Patient Centric” systems that act as ‘Islands of Excellence’ providing quality cost-effective treatments.

Conventional Wisdom

Over the past few years the pharmaceutical industry has viewed Physicians as one of the dominant entities influencing its success and growth. A physician reserved the autonomy on decisions concerning the choice of therapy for his patients and was subjected to influence mainly by peers (group-practices) and Industry leaders (KOLs). Consequently, all pharmaceutical companies focused their promotional and educational initiatives on physicians. Sales teams were determined to acquire the mind share of physicians which resulted in having to tap a large group of individuals in order to expect returns. However, this is becoming old school.

The Evolving Industry

In the recent past, Health Care providers (primarily hospital chains) have undergone a series of vertical and horizontal integrations. Vertical integrations included the acquisition of primary care physicians (PCPs), strategic alliances with physicians in physician-hospital organizations (PHOs) etc. On the other hand, horizontal integrations involved the establishment of multihospital systems, alliances with neighboring hospitals and mergers. Over time, such integrations have evolved and enhanced to what is today referred to as the Integrated Delivery Network (IDN).

The integrations have resulted in the creation of a network of facilities and providers working together to offer a continuum of care. Prevailing economic market conditions and an array of healthcare reforms demands high quality of treatment at reduced costs (PPACA -2014). The very nature of integration allows IDNs to gain perspective on quality and cost factors that lead to better outcomes. This new vision focuses not only on intervention, but also on prevention and wellness, guiding patients to the most appropriate site of care, at the right time and cost. In short, IDNs are “Patient Centric” systems that act as ‘Islands of Excellence’ providing quality cost-effective treatments.

rob halkes's insight:

In short: The world of health care is changing rapidly under the stres of more quality and volume for less costs of care. The formation of Integrated Delivery Networks (IDNs) will rise. To the health industry and pharma it means: if ou're not in, you're out and your competitor is in. This makes the need to change principles of market approach from a pharmaceutical company even higher.

To get content containing either thought or leadership enter:

To get content containing both thought and leadership enter:

To get content containing the expression thought leadership enter:

You can enter several keywords and you can refine them whenever you want. Our suggestion engine uses more signals but entering a few keywords here will rapidly give you great content to curate.

Your new post is loading...

Your new post is loading...

More insight into pricing of medicines.

Here's a new report on the factors influencing drug expenditure, including the issues around pricing. It surely helps politicians and other stakeholders to understand the complexity of the pricing process pharma companies see themselves confronted with.

The Quintiles_IMS_insitute published a report on the drivers of drug expenditure in the U.S.

"Much of the coverage on list prices has left out the more complex context of the prices, including

I must state: obliged reading for policy makers, insurers, pharmacy benefit managers and other healthcare stakeholders, including journalists (!)

See here: http://quintilesimsinstitute.org/files/web/IMSH%20Institute/Reports/QIIHI_Understanding_the_Drivers_of_Drug_Expenditure_US.pdf

And, still this is not the whole story, of we also look at regulations to access to markets, including reimbursement ruling and influences of reimbursement models/schemes like pay for performance and population health, as well as preference schemes for medicines by medical committees or payer incentives...